Monday, May 7th

Consumer credit outstanding increased at a 6.7% annual rate or by $13.5 billion in March. Consumers used credit cards and took out car loans at an almost equally fast pace in March as mortgage equity withdrawals decreased. Credit usage is expected to remain elevated as consumers use other lines of credit to finance spending due to weakening in the housing market and slower cash out refinancings.

Tuesday, May 8th

The NAR lowered their forecasts for home sales and prices again this month after a similar sized downgrade last month. The Association expects existing home sales to decline 2.9% this year to 6.29 million compared with its April sales forecast of 6.34 million. New home sales are now expected to drop 18% to 864k, vs. the earlier forecast for a 14% decline. In its first ever projected price decline, the NAR said that prices for existing homes will fall 1.0% this year while new home prices are expected to remain unchanged. Forecasts of 2008 existing and new home prices are for gains of 1.0% and 2.0% respectively.

Wednesday, May 9th

The MBA mortgage applications index rose 3.6% to 680.7% for the week that ended May 4. The purchase index climbed 2.6% higher on the week while the refinance index gained 4.9%. After falling steadily from mid-2005 though 2006, home purchasing activity has stabilized in the last 5 months. Refinancing activity continues to surge as many homeowners facing resets in adjustable rate mortgages are opting to refinance into a more favorable loan.

The FOMC opted to hold the target for the fed funds rate steady at 5.25% at their policy meeting today. This was the seventh straight meeting policymakers have left rates alone. Moreover, there were only minimal changes to the post-meeting statement. The Fed acknowledged slower growth in the first part of this year and that recent indicators have been mixed. They stated again that the correction in the housing market was ongoing and forecast moderate economic growth ahead. The Committee reiterated that core inflation remained somewhat elevated but that they were optimistic that inflationary pressures would moderate. The current high level of resource utilization poses an upside risk to inflation. The Fed maintained that inflation continues to be the predominate risk to the economy and that future policy adjustments will remain dependent upon incoming economic data.

Thursday, May 10th

Import prices jumped 1.3% in April led by a 6.5% gain in petroleum prices. Excluding petroleum, import prices rose just 0.2% on the month. Overall import prices gained 1.9% over the past year.

The international trade deficit jumped to $63.9 billion in March from a shortfall of $57.9 billion in February. The trade gap widened because of a 4.5% surge in imports. Exports increased 1.8% on the month. The wider trade gap will detract from Q1 GDP in subsequent revisions.

Jobless claims fell 9k to 297k for the week that ended May 5. The four week moving average, used to smooth out weekly volatility, also fell 12k to 317k. The low level of claims is consistent with tight labor market conditions.

Friday, May 11th

Retail sales fell 0.2% in April, much lower than an expected gain of 0.4%. However, retail sales were upwardly revised in March from a gain of 0.7% to an increase of 1.0%. Sharp declines in sales of motor vehicles, building materials, clothing and general merchandise weighed down overall sales. Excluding motor vehicles, core retail sales also fell 0.2% on the month. Consumer spending was weak in April but is still expected to grow modestly in coming months.

The producer price index jumped 0.7% in April as energy prices shot up 3.4%. The PPI was up 3.2% over the last year. Excluding food and energy from the index, core consumer prices were unchanged in April and gained a moderate 1.6% over the last year. Core wholesale inflation remains contained at this time but the headline figure remains a concern due to the pass through of energy prices.

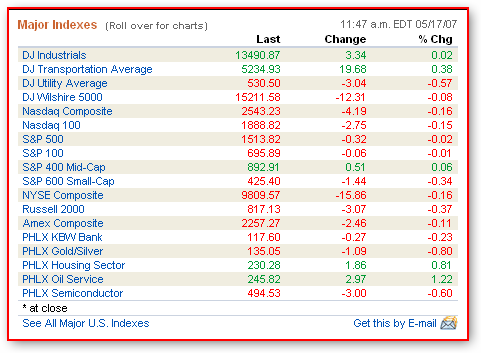

Stock Market Close for the Week

Index Latest A Week Ago ChangeDJIA 13326.22 13264.62 +61.60 or +0.46%

NASDAQ 2562.22 2572.15 -9.93 or -0.38%

WEEK IN ADVANCE

More inflation and housing market data on tap this week. Financial markets will be looking for the consumer prices index to support an easing inflation outlook and housing starts data to point toward some stabilization in new home construction. Also, Fed Chief Ben Bernanke will discuss the subprime mortgage market Thursday, in Chicago.

Key Interest Rates Latest 6 Mos Ago 1 Yr AgoPrime Rate 8.25% 8.25% 7.79%

Fed Discount 6.25% 6.25% 5.79%

Fed Funds 5.25% 5.24% 4.84%

11th District COF 4.299% 4.382% 3.624%

10-Year Note 4.67% 4.64% 5.14%

30-Year Treasury Bond 4.85% 4.74% 5.22%

30-Yr Fixed (FHLMC) 6.15% 6.33% 6.58%

15-Yr Fixed (FHLMC) 5.87% 6.04% 6.17%

1-Yr Adj (FHLMC) 6.76% 5.55% 5.62%

6-Mo Libor (FNMA) 5.3581% 5.3898% 5.2879%

Sources: IBC' s Money Fund Report; Bank Rate Monitor; Federal Home Loan Bank of San Francisco

If you enjoyed this post, take a few seconds of your time and

subscribe to our RSS feed. CFL Real Estate News is updated daily.